SMSF portfolios are 'upside-down'

In accumulation phase, when contributions are being piled into super in all efforts to boost the capital available at retirement, it makes sense to concentrate on growth assets. They may be more risky but there’s a better chance of higher returns, and higher returns will compound to a higher balance.

In pension phase growth assets are still worth holding, but portfolios are often weighted towards lower-risk assets, or a no-risk asset like cash.

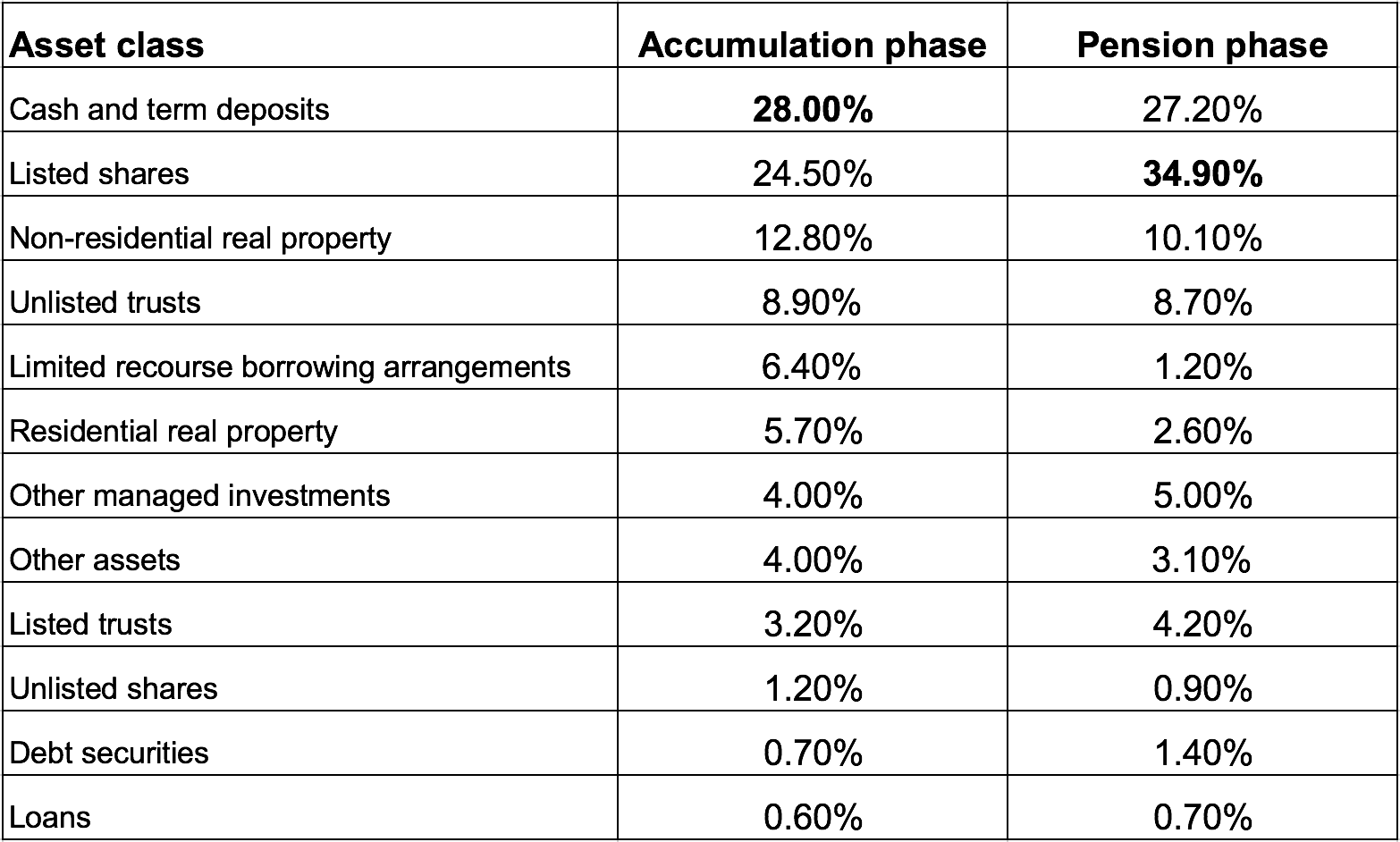

Well, it looks like no-one has told DIY super fund trustees because data from the Tax Office for the year to June 2014 (the latest annual numbers available) show the most favoured investment in accumulation phase is cash, and in pension phase it’s listed shares.

The table shows the proportion of assets held by SMSFs in accumulation and pension phase, as reported to the ATO in 2014.

The strategy looks risky from two angles. Firstly, these funds are missing out on the possibility of higher returns from listed shares in the lead up to retirement when an overweight position in equities has been shown to work. That big cash balance could be put to better use, for sure.

Secondly, although they maintain a high cash weighting in pension phase their allocation to shares has increased from 24.5% to 34.9%, making portfolios more prone to market risk at a time when regular withdrawals are mandatory.

It seems a bit upside-down.

A better balance

The data shows a snapshot of all SMSFs rolled into one, but some DIY super portfolios are much more sophisticated than others. Still, it is clear something is not right. If this is how the average DIY fund is invested, it would do better to reverse its accumulation and pension phase allocations to cash and shares. An opposite strategy to the current one would lead to a better result.

Is there an easier way? There is, if the trustees feel it’s OK to relinquish a bit of the control and choose to invest in a model portfolio.

The InvestSMART model portfolios, for example, are rebalanced periodically on the advice of professional investment consultants. The portfolios are highly diversified, holding thousands of individual companies within exchange-traded funds. Some of these funds, or ETFs, hold Australian listed stocks but others are dedicated to global markets. Another shameful secret of DIY funds is that they are woefully under-invested in offshore markets (the numbers for global assets in the ATO data are so small they have been combined with five other investment classes and relegated to “other assets”).

Control and common sense

Most SMSF trustees (59%) say they set up their own super funds because they “wanted control and choice over their investments”, according to research from the Financial Services Council.

There’s nothing wrong with that, but the allocations data here shows some of them need help. They would be better off passing the portfolio construction task on to someone else. A model portfolio that is rebalanced regularly and maintained by professional investment consultants will beat the average SMSF portfolio as reported by the ATO any day.

Frequently Asked Questions about this Article…

SMSF portfolios appear upside-down because many trustees favor cash in the accumulation phase and listed shares in the pension phase. This is contrary to the typical strategy of focusing on growth assets like shares during accumulation for higher returns and shifting to lower-risk assets in the pension phase.

Holding a high cash balance in the accumulation phase can be risky because it misses out on the potential higher returns from equities. This strategy may not maximize the growth of the retirement fund, which is crucial during the accumulation phase.

In the pension phase, increasing the allocation to shares from 24.5% to 34.9% exposes the portfolio to more market risk. This is concerning because regular withdrawals are mandatory, and market volatility can impact the fund's stability.

A better strategy would be to reverse the current allocations: focus on growth assets like shares during the accumulation phase and shift to lower-risk assets like cash in the pension phase. This approach aligns with maximizing growth early and preserving capital later.

Trustees can improve their strategy by considering model portfolios managed by professional investment consultants. These portfolios are diversified, periodically rebalanced, and can provide better results than the average DIY SMSF portfolio.

SMSFs are under-invested in global markets because many trustees prefer domestic investments. The ATO data shows global assets are so minimal they are combined with other investment classes, indicating a lack of diversification.

Using a model portfolio offers the benefit of professional management, regular rebalancing, and diversification across thousands of companies. This can lead to better performance compared to the average SMSF portfolio.

Most SMSF trustees prefer managing their own funds because they want control and choice over their investments. However, the data suggests that some trustees could benefit from professional guidance to optimize their portfolios.