Is There a Future for Buy Now, Pay Later?

It’s not only tech stocks and crypto assets that have tanked in the face of significant macro headwinds. The once ascendant buy now, pay later (BNPL) sector has finally come a cropper, replete with broken deals and sinking share prices.

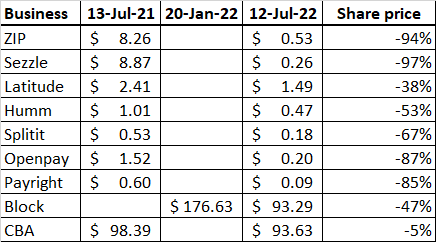

Investors who bought into the sector in mid-2021 are now facing significant losses in most cases. Afterpay investors may consider themselves fortunate to have been provided a lifeline from Block (formerly Square) in late 2021, although investors who remain invested are still seeing a paper loss of 47 per cent as of writing compared to the Block share price in January. Proposed deals between Zip and Sezzle and Latitude and Humm have also fallen through.

Source: https://www2.asx.com.au/

The question facing investors at the moment is what, if anything, has changed about the prospects for BNPL providers, and do current prices reflect simply a short-term market sentiment change or a more systemic challenge to the fundamentals?

To assess this, it’s useful to understand how a BNPL service rewards or penalises each participant in the payment flow.

- Consumers approved by the BNPL provider can typically split a payment for a specific transaction into instalments over a short-term period of weeks or months. If instalment payments are made in time, then no (or fewer) charges apply. But if the consumer is late in covering an instalment, then a penalty fee may be charged. Consumers may more easily obtain approval for a BNPL service compared to a traditional credit card service.

- Merchants offering the BNPL service to their consumers pay service fees to the BNPL provider, typically based on the transaction amount, cents “per transaction”, or potentially both. Merchants theoretically benefit from increased shopper traffic arising from their visibility in the BNPL “ecosystem”.

- The BNPL provider earns fees from the merchant for all transactions processed via BNPL and typically also the consumer where the consumer is late in making instalment payments.

BNPL provider revenue flow therefore relies upon:

- Consumers signed up and approved to use the BNPL service.

- Merchants signed up and approved to use the BNPL service as a payment acceptance method.

- Consumers purchasing goods and services at those participating merchants.

- Consumers using BNPL as a payment method, triggering merchant fee flow to the BNPL provider.

- Consumers missing instalment payments, triggering consumer fee flow to the BNPL provider.

During periods of economic growth, BNPL providers get a tailwind as volumes increase across the board. Competition from other BNPL providers can deny a BNPL provider from capturing a particular merchant’s business, but in general a rising tide lifts all boats.

But in a tougher economic environment, revenues can come under pressure from all sides:

- Diminished consumer sentiment due to rising interest rates, inflation fears etc leading to reduced shopping related payment volumes.

- Competition from alternative payment methods including credit cards, debit cards, charge cards (eg. Amex, Diners), mobile wallets (eg. AliPay, WeChat Pay) and cash.

- Competition to retain merchants and consumers from leaving for other BNPL providers.

- Consumers increasing their propensity to make their instalment payments on time which reduces late payment fees to the BNPL provider.

- Regulatory constraints (currently, BNPL advances are not captured under existing consumer credit legislation).

Consumers less likely to qualify for a credit card are attracted to BNPL due to the lower approval thresholds. But such consumers are also more likely to curtail spending when circumstances change as well as fail to make penalty payments due to an inability to pay.

Pressure on the merchant side comes from competition either driving fee margins lower, or conversely prompting fee increases to drive extra margin in the face of lower volumes, which at some point results in merchants leaving due to dissatisfaction with the fees. This becomes a vicious circle from which escape is difficult.

Despite this, BNPL’s emergence has changed the landscape. “TradFI” (shorthand for “traditional finance”) players have been tempted to get on board, with the likes of Visa, MasterCard, Paypal and several banks all offering, or looking to offer, their own takes on BNPL. Some of these approaches look more like consumer credit with a revolving interest component while others adopt the approach of an instalment plan with fee.

Given the current downturn in fortunes of the first wave of BNPL challenges, it remains to be seen how successful the second wave will be. It would be unsurprising to see some players disappear from the scene, either via merger and/or acquisition or simply closure due to insolvency.

Brave investors with a longer-term view might consider current price action to represent a buying opportunity. Risks abound, but BNPL is likely to remain a viable payment method amongst a certain consumer demographic.

Frequently Asked Questions about this Article…

The BNPL sector has faced significant challenges recently, with many companies experiencing falling share prices and broken deals. Investors who entered the market in mid-2021 are now facing substantial losses. Despite these setbacks, BNPL remains a viable payment method for certain consumer demographics.

BNPL providers earn revenue through fees charged to merchants for transactions processed via their service and from consumers who miss instalment payments. The revenue flow depends on the number of consumers and merchants signed up, as well as the volume of transactions processed using BNPL.

BNPL providers are facing challenges such as diminished consumer sentiment due to economic factors like rising interest rates and inflation fears, increased competition from alternative payment methods, and regulatory constraints. Additionally, consumers are more likely to make instalment payments on time, reducing late payment fees for providers.

Consumers might prefer BNPL over traditional credit cards because BNPL services typically have lower approval thresholds, making them more accessible. This is particularly appealing to consumers who may not qualify for a credit card.

While the BNPL sector is currently facing downturns, some investors with a long-term perspective might see the current low prices as a buying opportunity. However, risks remain, and the future success of BNPL providers will depend on their ability to adapt to economic challenges and competition.