25 experts share their top money tip for 2025

Most people see the new year as a great opportunity to make a fresh start. We wanted to help you start 2025 right, so we asked 25 financial experts for their top wealth-building tip for the year ahead. Check out their responses.

John Addis: Be patient

Crazy multiples are everywhere, from tech stocks like Pro Medicus and WiseTech to Commonwealth Bank, which has never been more expensive. Kitchen filler Breville and plumbing outfit Reece are both on 38 times future earnings and Australia's most incompetent monopolist, the ASX, is on 26 times future earnings.

There is a point of capitulation near the top of the market as well as the bottom. The formerly bearish US banks JPMorgan and Morgan Stanley recently rolled over and joined the fevered crowd. This is often a sign of it, as is my local servo dispensing Bitcoin but not selling Nobby's Nuts.

When everyone else seems to be making a killing, doing nothing is hard. But it is also what successful investing requires. Patience is my tip for 2025. Although human nature is not on our side in these moments, history usually is.

John Addis is the founder and Editor of Intelligent Investor.

Cate Bakos: Have an end game in mind when buying property

Having an end game is critical. Many property investors who get started aren't clear on their debt reduction strategy. It is this strategy that determines the investment approach. Is the end game one of 'buy and hold' or is the investor planning to crystallise a gain and reinvest the profits into a liquid asset? The difference between living off rental proceeds and relying on dividends is significant and underpins the types of properties (and the number of properties) held in the portfolio.

Determining the end game also requires an understanding of borrowing capacity constraints and relevant purchase timing. Those who procrastinate or wait for conditions to change often have regret in later years when their inaction translates into a lost opportunity.

In 2025 especially, delaying the investment process in an attempt to time the market or predict interest rate movements may lead to regret if competition heats up before a purchase is made.

Cate Bakos is the founder of Cate Bakos Property, a boutique and independent Melbourne Buyers Agency firm and co-host of The Property Trio podcast

Nathan Bell: Recognise the difference between luck and skill

Some parts of the stock market have become divorced from reality, particularly since the US election. The Australian banking and tech sectors hold many stocks that are drastically overvalued but show no signs of slowing down.

If you're lucky enough to own any of these market darlings, the best thing you can do is recognise the difference between luck and skill and make sure you lock in the lucky gains where the company has little hope of meeting Mr Market's lofty expectations.

Valuations for many stocks are currently at records that may never be repeated, so make sure you cash in and maximise your luck by reinvesting in the numerous options that don't require unrealistic assumptions.

Nathan Bell is Head of Research & Portfolio Management at Intelligent Investor.

Mark Chapman: Remember paperwork is king

When it comes to tax time, keeping your paperwork is king. Remember to keep all receipts and invoices for expenses you think could be tax-deductible. You must have a copy of the receipt or invoice for almost all deductions you wish to claim (with a few very limited exceptions). I've seen many people knocked back by the ATO when they try to claim something and can't prove that they spent the money on a work, business or investment-related expense. So, to maximise your refund, use the remainder of the tax year to get your paperwork in order.

Mark Chapman is Director of Tax Communications at H&R Block Australia.

Paul Clitheroe: Spend less than you earn

Sure, I know this is super basic. But too few of us follow the basics. The best money tip ever is to spend less than you earn. That is followed by investing on a regular basis. Quite frankly, as long as you are doing these two things, I don't care much where you invest the money. It is the habit of saving that creates wealth.

It may be paying off a credit card debt, your mortgage, topping up super or adding to your share portfolio. All of these work brilliantly in the long term. Please remember that just $5 a day, invested sensibly throughout your working life, would add about $250,000 in today's money to your future capital. There is so much rubbish written about building wealth. The tips above, plus a true miracle of money, compound returns, are how most of us will, in time, become financially independent.

Paul Clitheroe AM is Chairman of InvestSMART and one of Australia's leading personal finance media commentators.

Eric Dickler: Factor in the potential tax outcomes when investing

Careful consideration should be given to the tax impacts and/or benefits when you formulate your investment strategy and decide on your holding periods. In Australia, if an individual investor holds on to shares or ETFs for more than 12 months, then the investor is entitled to a 50% capital gains tax (CGT) discount which helps you keep more of your investment profits in your pocket.

If you hold your investment for less than 12 months, then the gains are not discounted and are taxed at your marginal tax rate.

By incorporating tax planning into your investment strategy, you can make informed decisions that align with your goals, whether you're aiming for quick liquidity or long-term growth. Always factor in the potential tax outcomes to maximise your after-tax returns.

Eric Dickler is the co-founder of EDR Accounting & Business Solutions.

Andrew Dunbar: Invest in yourself

Your future earning potential is likely to be your single biggest asset. A 45-year career at today's average wage would see you bringing in around $3.7 million, and there are options to grow this figure if you are prepared to invest in yourself.

Take a look at job advertisements for roles at the next level to see what skills employers are looking for and work out what you need to do to build them. Whether it's education, skills training or networking, these investments can increase your value in the job market, leading to higher earning potential over your lifetime. Working out what you want to do with your career and how you can get there will put you on the path to the ultimate goal - financial freedom.

The benefits of professional development extend beyond financial gain; they enhance your overall wellbeing, relationships and future prospects. Ultimately, investing in yourself creates a foundation of success that can outperform most conventional investments. And those conventional investments will be far more powerful when you are able to devote your resulting higher earnings towards them.

Andrew Dunbar is Director and a Senior Financial Planner at Apt Wealth Partners.

Bianca Hartge-Hazelman: Avoid selling property

My number one tip is to avoid selling property for as long as possible. If you are struggling with mortgage debt, then look to see how you can make it work to meet that debt before selling out. Can you let a room out for instance? Financial pressures come and go and it's staying the course that often makes for the best financial sense in the long term.

Bianca Hartge-Hazelman is the CEO of Financy and author of the Financy Women's Index.

Pascale Helyar-Moray: Add as much as you can to your super

Your secret to superannuation success is based on the principle of maximum contributions, with minimum effort. If you're not already salary sacrificing into super, it's worth considering. Even a small amount can make a big difference to your balance at retirement. All you need to do is write a two-sentence email to your payroll manager to make this happen.

While you're at it, why not set up a direct debit from your bank account into your super as a voluntary contribution? In automating this, you're making life really simple for yourself. And if you schedule the direct debit into your super to take place on payday, you won't miss the money - or be tempted to spend it.

Pascale Helyar-Moray OAM is the founder of Grow My Money, a cashback platform that pays cashback directly into your super or home loan.

Ron Hodge: Spend less, save more and don't put all your eggs in one basket

My top financial tips never really change from year to year. It's the same advice my parents gave me when I was young: spend less, save more and don't put all your eggs in one basket. Over my nearly 30 years in financial markets, this simple message always holds true and goes much deeper than most expect.

It is not just about spending less on frivolous stuff, it is also about making sure you are paying the lowest prices for major necessary expenses such as your mortgage, insurance and investments. Lower costs mean more money in your pocket. A new financial year is always a good time to review your major expenses and make sure you are getting value for money.

More money in your pocket means you have more money to invest and build wealth over time. And remember, don't put all your eggs in one basket - diversification is key. Spread your money across investments in various asset classes, including cash, bonds, equities, and property.

Also, keep in mind that if the returns promised on an investment seem too good to be true, they usually are. Tell them they're dreaming or at worst crooks and walk away!

Ron Hodge is CEO of InvestSMART Group.

Jessica Irvine: Focus on what you can control

My top money tip for 2025 for all investors is to shut out the noise and focus on what you can control. No individual investor can influence market outcomes. All we can control is our mindset, our cash flow and putting in place adequate protections for our portfolios, including being adequately diversified, meaning not all our eggs are in one basket.

Create a budget and track your spending to make sure you are maximising the leftover cash flow you have to invest in the first place. Review your insurance and bigger bills and reflect on your daily spending to make sure it is in alignment with the life you are investing to create. Even small tweaks to your spending habits can add up over time and turbocharge your ability to grow your wealth.

Jessica Irvine is CommBank's Personal Finance Expert.

Glen James: Know your why

Wealth-building starts with knowing your strategy and your 'why.' Are you investing to retire early, fund your child's education, or save for a dream holiday? Once clear on your goal, determine how much of your spending can be allocated to it. A solid emergency fund and spending plan are key - they ensure you can confidently commit a set amount to wealth creation each week, month, or year.

Next, decide on the right structure for your investments. Most people will invest in their name, but options such as joint names, superannuation, trusts, or bonds might suit more complex goals.

Finally, automate your investments to remove human error and let them grow uninterrupted. Investing is a slow, steady process - it might not be exciting, but it works.

My top tip for 2025 is to make sure your strategy comes first, then plug in your investing regularly.

Glen James is host of the money money money (formerly my millennial money) & Retire Right podcasts and author of The Quick-Start Guide to Investing.

Alan Kohler: Be careful with risk and tax when investing

Consider risk and tax. When it comes to risk, think about it in terms of your 'risk-free rate', which is not the 10-year bond rate used by professionals. For you, it's the highest 12-month term deposit rate with a bank, currently around 5%, which is government-guaranteed up to $250,000 for each account. How much more than that do you want for taking risk? The 50-year total return of the S&P/ASX 200 is 6.1%. Is 1.1% extra enough? This is a personal decision for you alone.

Then there's tax. Investment returns are not all yours - you're in an investment partnership with governments, and never forget it. For example, the difference in the end result between a land-taxed real estate investment and 100%-franked company share is enormous. Always figure it out.

Alan Kohler AM is the founder of Eureka Report and host of The Money Café podcast.

Peter Koulizos: Sacrifice to build wealth

My top tip for creating wealth is sacrifice. Basically, you need to sacrifice the opportunity to spend money now so that you have even more money in the future. The two main forms of sacrifice are saving and investing.

You need to start by saving some of the money you earn, rather than spending it all. If you're a teenager or young adult with a part-time job, saving at least 10% of your income should be your goal. If you are in full-time employment, you should aim to save as much as 30% to 40% of your income.

Once you have saved some money, then you can start investing. The two main investment vehicles are the share market and property. If you have saved up a few thousand dollars, investing in blue chip shares can be a great option. If you have been a disciplined saver over many years and have saved tens of thousands of dollars, consider buying property, especially your own home.

Peter Koulizos is a property lecturer at The University of Adelaide.

Margaret Lomas: Get on the property ladder by becoming a landlord first

In 2025, breaking into the property market in Australia's major capital cities can seem impossible. Instead of saving for years to buy a home in these expensive areas, consider becoming a landlord first. By purchasing cheaper houses or units in smaller capitals or regional areas, you can start building your property portfolio sooner.

Look for properties in areas with strong fundamentals and good cash flow to ensure most expenses are covered. This way, you can continue saving towards your own home while your tenant covers your mortgage and expenses.

Over time, as you build a small portfolio of investment properties and accumulate additional savings, the increasing equity in these properties can provide extra funds once sold, boosting your deposit for that dream home in the area you want to live. By thinking outside the box, investing wisely, and having some patience, you can turn the dream of homeownership into a reality.

Margaret Lomas is a qualified financial and investment property adviser and the founder and director of Destiny Financial Solutions.

Diana Mousina: Just do it

"Just do it". This saying is relevant to a long-term investor because the opportunity cost of not doing it (i.e. investing) probably carries more downside because you lose the benefits of compound interest.

Inevitably, investing carries risks. Share markets are volatile. In Australia, just under half of all trading days have negative returns. However, over the long term, 80% of years have positive returns and 100% of decades have positive returns. This is worth keeping in mind as a long-term investor - especially as timing the market is basically impossible.

An investor who was fully invested in the Australian All Ordinaries Accumulation Index from 1995 would have returned an average of 9.5% a year. If you managed to time the market and missed the 40 worst days in the share market this return would have nearly doubled to 17%. On the flip side, if you missed the 40 best days, the return would have fallen to just 3.5%.

Diana Mousina is Deputy Chief Economist at AMP.

Owen Rask: Explore ETFs for passive income for retirement

If you have created wealth using property and you're thinking "I want more passive income" the writing is on the wall. It's time to start thinking about shares or ETFs to switch from 'active' income to 'passive' income.

I deal with hundreds of early retirees and thousands more who rely on super and retire 'on time'. What unites them is a strong understanding of the difference between active and passive income. Within passive income streams, Australian shares are a standout. You see, assets like property have lots of ongoing costs, such as tenancy management, land tax, interest costs and so on.

Ultimately, that's why negative gearing exists. But negative gearing, and using residential property for retirement generally speaking, is a very sub-optimal retirement plan.

Shares and ETFs offer low ongoing fees, no maintenance, tax-effective franking credits, liquidity and diversification, making index ETFs perfect for passive income seekers. I estimate it's the difference between negative income (from an all-property portfolio) and 3-5% (diversified using ETFs across Aussie shares and other markets). I know which I'd rather retire on.

Owen Rask is the Chief Investment Officer of Rask Invest and Founder of Rask. He hosts a number of podcasts including Australian Investors Podcast and Australian Finance Podcast.

Michael Saliba: Consider using a family guarantee to fast-track your property investment journey

Did you know a family guarantee could help you fast-track your property investment journey? While commonly used by first-home buyers, this strategy can be a hidden gem for aspiring investors.

A family guarantee allows you to leverage the equity in a family member's home - typically parents - as security for your loan. This means you can purchase an investment property without needing a deposit and avoid costly lenders mortgage insurance.

By using a family guarantee, you can enter the market sooner, potentially benefit from capital growth and preserve your savings for other investments. Once your property increases in value, you can refinance, remove the guarantee and even use the equity for future purchases.

A good mortgage broker can help you structure the loan responsibly and protect your guarantor. With the right guidance, this strategy can be a game-changer for building long-term wealth.

Michael Saliba is a mortgage broker at Mortgage Choice.

Phil Slade: Automate your savings and investments

The one big tip I have for building financial wealth in 2025 is to automate savings and investments as much as possible.

This helps overcome 'Present Bias' (the tendency to prioritise immediate gratification over long-term financial goals), reduces decision fatigue, leverages mental accounting (using separate accounts to mentally allocate funds for specific purposes), and harnesses the power of defaults.

Some good ways to do this include:

- Setting up automatic transfers from your income account to a savings account or investment portfolio. Start with a reasonable percentage of your income, such as 5%, and gradually increase it over time.

- Consider using 'round-up' apps that automatically save small amounts with each purchase.

- Align your automated savings with specific financial goals to increase motivation.

By making saving and investing automatic, you use the power of inertia and habit formation to work in your favour.

Phil Slade is a behavioural economist, co-founder of Decida and co-CEO of Switch4Schools.

Caroline Stewart: Discuss money as a family

Open, honest conversations about money can help build the financial wellbeing of all members of your household, regardless of their age. Whether it's a teen getting their first job, a young adult deciding how to invest, or a parent or carer planning for long-term security, everyone benefits from understanding how to make informed financial choices.

In an increasingly digital world where social media and finfluencers often seem to have an outsized impact, it's important to discuss that those promotions may not be the best fit for your family's needs or financial goals.

Encourage teens and young adults to be critical thinkers by questioning the content they see online, disclosures about sponsorships, advertised returns and always compare information from a range of trusted, reliable sources.

Good money decisions often require time, research, and some patience. Instead of following the latest trends or the newest investment scheme, households can apply healthy scepticism and weigh up the risks and rewards, all essential life skills for managing money.

Caroline Stewart is CEO of Ecstra, a not-for-profit organisation committed to building the financial wellbeing of all Australians.

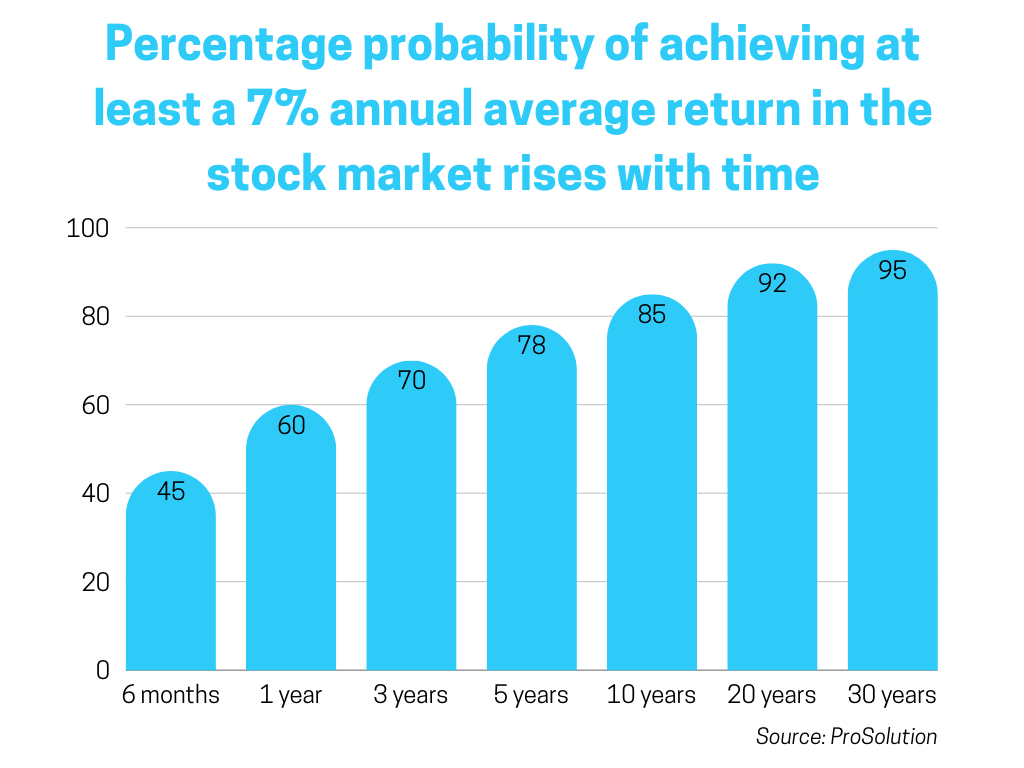

Stuart Wemyss: Play the long game

My number one tip for 2025 is to ask yourself: "What can I do this year that has the highest probability of putting me in a stronger financial position in 10 years' time?"

The key is to 'play the long game'. Too often, investors chase short-term gains, but these rarely create enduring value. Instead, focus on sound fundamentals and strategies with compounding potential, such as investing in high-quality, long-term assets like investment-grade property or a diversified ETF. This approach benefits from reduced taxes, lower risk, and (hopefully) exponential growth over time.

Discipline and patience are essential. Ignore the noise of quick-win opportunities and stay committed to your long-term strategy. While it may not be as exciting in the moment, this is the most effective way to build significant wealth and financial security.

Stuart Wemyss is the founder of boutique financial services firm ProSolution Private Clients.

Tom Wilson: Keep things simple

One of the most common mistakes investors make is believing that complex strategies lead to better results. But the truth is that complexity often works against you. The investors who consistently achieve the best outcomes keep their approach simple: diversified portfolios aligned with their goals, risk tolerance and timeframes.

Here's the insider knowledge: complexity isn't just risky, it's exhausting. Whether it's trying to time the market, predict currency movements, or chase high-flying stocks, these approaches often lead to emotional decisions, unnecessary costs, and underperformance. Even strategies that sound sophisticated, such as options trading or leveraging property, can expose investors to outsized risks and unpredictable outcomes.

The smart money focuses on what works. A straightforward, diversified portfolio allows compounding to do the heavy lifting and frees you from the stress of trying to outsmart the market. Sometimes, the best move is to take a step back, simplify, and trust the process.

Tom Wilson is an Investor Educator at InvestSMART and runs Bootcamp for Beginners, an online course designed to teach the basics of financial literacy and investing.

Andrew Yee: Make sure you're getting the most from your SMSF

If you have a self-managed super fund (SMSF) make sure that you are getting the most out of it. To achieve this goal, there are three main considerations:

1. Super and tax laws. It's important to be aware of the rules about your SMSF, not only from a compliance perspective but also from a strategic perspective.

2. Your investment strategy. Review your investment strategy and adjust if required. Is the fund properly diversified? Is there too much cash (or not enough) held in the fund?

3. Take advantage of the tax benefits. Make sure you make the most of all the tax benefits available to superannuation, such as maximising concessional (tax-deductible) contributions, or paying tax-free pensions to the members.

Finally, always seek professional assistance to advise and administer your SMSF.

Andrew Yee is an SMSF specialist and tax accountant.

Effie Zahos: Have a monthly 'life admin' session

Set aside one hour each month in your calendar for a 'life admin' appointment. It's a simple habit with the potential for big payoffs for your finances. Even if you don't always use the full hour, the act of committing ensures you stay on top of the little things that often get overlooked.

Start by tackling the basics: set up your myGov account properly, add your Medicare card to your phone, organise your passwords, add loyalty cards to your digital wallet. You get the idea ...

You can also use the time to check in on your budget, cancel unused subscriptions, or ensure you're getting the best rates on savings or loans, energy or mobile plans.

This regular check-in keeps you organised, reduces financial stress, and ensures nothing slips through the cracks. It's like a monthly tune-up for your financial health - short, simple, and surprisingly effective.

Effie Zahos is a Director of InvestSMART and 9News Money Editor.

Angel Zhong: Master your money mindset

Looking ahead to 2025, a powerful wealth-building strategy isn't just about picking the right stocks or timing the market - it's about mastering your money mindset. Start by conducting a thorough 'lifestyle audit': track every subscription, review all insurance policies, and scrutinise recurring expenses. You'd be surprised how many people lose thousands annually to services they barely use or premiums they could negotiate down.

This isn't about extreme budgeting; it's about redirecting money that's quietly leaking from your wealth-building potential. Once identified, direct these recovered funds into investments automatically. Remember, a $50 monthly subscription cancelled and invested instead could grow to over $100,000 in 30 years at a 7% return. In a world obsessed with finding the next big investment opportunity, the real wealth often lies in plugging the small leaks in your financial boat.

Dr Angel Zhong is Associate Professor of Finance at RMIT.

Frequently Asked Questions about this Article…

John Addis advises investors to be patient in 2025. He emphasizes that successful investing often requires doing nothing, even when others seem to be making quick gains. Patience, he suggests, is supported by historical trends.

Cate Bakos highlights the importance of having an end game in property investment. Knowing whether your strategy is 'buy and hold' or selling for reinvestment helps determine your investment approach and manage debt effectively.

Nathan Bell suggests that recognizing the difference between luck and skill can help investors lock in gains from overvalued stocks. By understanding this distinction, investors can reinvest in opportunities that don't rely on unrealistic assumptions.

Mark Chapman stresses the importance of keeping receipts and invoices for tax-deductible expenses. Proper documentation is crucial to maximize tax refunds and avoid issues with the ATO.

Paul Clitheroe advises that spending less than you earn and investing regularly are fundamental to wealth-building. This habit, combined with compound returns, can significantly enhance financial independence over time.

Eric Dickler recommends factoring in tax impacts when planning investments. Holding shares for over 12 months can provide a 50% capital gains tax discount, maximizing after-tax returns and aligning with long-term goals.

Andrew Dunbar emphasizes that investing in personal development can increase your earning potential, which is often your biggest asset. Skills training and education can lead to higher lifetime earnings and financial freedom.

Bianca Hartge-Hazelman advises against selling property hastily due to financial pressures. Exploring options like renting out a room can help manage mortgage debt, as staying the course often makes better financial sense in the long term.